There is rumour among central bank circles, watchers and commentators where the FED will head the next quarters with its primary policy rate, i.e. the federal funds rate. Some observers suspect that the FED will likely increase its rate in the beginning of next quarter; while others argue that the zero interest-rate will and should last at least until the calender year 2011. The former attribute their judgment on recent indiciators, such as industrial production or survey forecasts of market participants on key aggregate variables. The latter reach their conclusion on the basis of past policy behavior of the FED given inflation and GDP forecasts by FOMC staff.

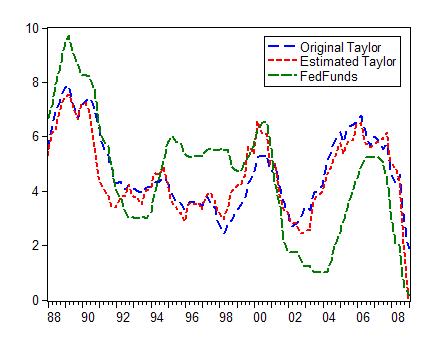

The Taylor rule is a proposal and a rough guidance for sound monetary policy. It basically states that the central bank should adjust its key rate by the formula below (first bullet). The rate should be 1.5 times inflation plus 0.5 times the output gap, plus 1. The blue line of the graph represents this normative statement.

Instead, many economists estimate the Taylor reaction function for different sample periods. Recently, Glenn Rudebusch , FED of San Francisco, has estimated such a rule for the period 1988q1:2009q1 to get parameter estimates for the inflation and output coefficients. These parameters describe how the FED reacted on average to inflation and output over the sample period. Using the estimated rule and applying internal staff estimates of future inflation and output, Rudebusch claims that the key rate should stay at zero for another two years (or even should become negative). I replicated his rule for the same period (with a slightly modified data set**). The estimated rule is represented by the red line and it largely hits the normative Taylor rule. Both rules considerably differe in 2002-2006 from the effective fedfunds, the rate under the control of the FED.

- Original Taylor: ff = p + 2 + 0.5*(p-2) + 0.5*y^gap

- Estimated Taylor ff = c + alpha*p + beta*y^gap with alpha=0.92, beta = 1.0 and c = 2.3

What is most important for the reader is that permamentley-updated rules are a poor guide where monetary policy should head. Why? Because amending such a rule with given coefficients for the future would perpetuate mistakes in the past. Just imagine, the FED would have followed the empirical reaction function derived from the pre-Volcker period 1960-1979. It is widely accepted that the monetary policy regime during this period was highly destabilizing becasue it did not follow the "Taylor principle" - a more than one-by-one reaction of the short rate to inflationary developments. Past mistakes, thus, would feed into present and future interest-rate decisions.

I highly agree with John Taylor that these recent mistakes were one major source leading up to the crisis (see the low reaction coefficient to inflation, alpha=0.92 vs. 1.5 in the Taylor rule). Sticking to a policy proposal of past FED behavior would bring about a recurrence of bubble history. This is definitely not what we seek for!

** I use the GDP deflator as proxy for inflation. If, instead, the CPI all itmes is applied, the Taylor rule would even suggest for the period 2002-2006 to keep the key rate even higher.